Our blog from the coal face of casino analytics

Stats and terms in this post

Slot free-play = promotional free bets issued to the players which need to be played at least once

Theo win = theoretical win or normalized revenues

Coin-in = gross volume of wagers (also called handle or turnover)

What you need to know

For decades casino managers considered buffets a forever loss maker. This assumption was upended with the opening of The Mirage where the buffet delivered consistent positive results. Might a similar upheaval occur with slot free-play? Recent academic scrutiny has illustrated that free-play offers deliver only tepid incremental benefits. Nonetheless, these programs persist and at times expand but rarely contract. Free-play addles crucial metrics such as slot hold, coin-in, and occasionally a player’s bankroll, thus obscuring results making analysis a nearly intractable challenge.

Successful programs, in our assessment, are those that have finely tuned their free-play initiatives to recoup the coupon’s face value while driving incremental frequency. We estimate that most properties have managed this feat. Data from four casinos we reviewed which included, over 4m play-days, indicate that $1 of free-play typically increases daily spend by ~$0.80, though results vary. Furthermore, a 10% increase in free-play issuance generally results in a ~7% rise in frequency. These outcomes vary (sometimes sharply) along lines of player value and competitive landscape. To boost the return on investment from free-play, we recommend a shift towards a more personalized approach, necessitating the adoption of AI to achieve at scale.

A hallowed tradition

Until 1989, a truism in the casino industry was that casinos needed buffets and they would always lose money. A paradigm shift—albeit in the most gluttonous sense of the term—occurred with the opening of The Mirage. Might there be a similar paradigm shift in that most hallowed of casino traditions: slot free-play (FSP)?

We read with great interest, and perhaps a bit of envy, Anthony Lucas’s recent publication on this topic, which continued a theme of tepid returns on free-play. Dr. Lucas’s research parallels our personal experience that free-play programs are often inefficient but needed, particularly in competitive markets. A platform ticket. We—the casino industry at large—have been watering with the free-play spigot for nearly half a century, and it is telling that there is still significant disagreement among well-informed executives about the role of free-play.

This post reviews the mechanics of free-play before proposing a framework for leveraging it to drive incremental gains. Lastly, we will review a basket of properties and evaluate the effectiveness of their free-play programs through the lens of the proposed framework.

Mechanics of how free-play changes on-day spend

Most slot systems—maybe all—are built around coin-in, win, and the product of those two numbers, which is almost universally called hold (for this post, we will further define slot win ÷ slot coin-in as coin-in hold). Any slot manager would know this trilogy intuitively. The protagonist of the first part of the free-play efficiency enigma (on day spend) is a lesser-known trilogy: win, slot drop, and drop-hold. Slot drop is loosely defined as cash buy-in plus purchased TITO tickets, and by extension, drop-hold is win ÷ slot drop.

To see how these measures interact, let’s consider the following example: When a player purchases, say, $100 in slot credit, her buy-in or contribution to the drop is $100, but her coin-in at that point is zero. When she begins to play, she starts with $100 on the meter. Assuming her average wager is $2, she will make 50 spins/bets to complete the first cycle of her buy-in. At the end of cycle one, coin-in will be $100, and if she is average, she will have lost approximately $8, beginning cycle two with $92 on the meter. This process typically repeats until she:

Exhausts her bankroll,

Hits a win objective, or

Hits a loss budget, or

Loses interest, or

Runs out of time.

For reference, typically, coin-in hold is around 8%, but win drop hold is 30% to 45%, implying the average patron cycles her initial buy-in around six times (30-45% ÷ 8% = ~6x).

From a player’s perspective, coin-in is an output, and free-play distorts how players arrive at the objectives outlined above. For instance: Too much free-play when a player loses interest or is time-constrained reduces buy-in cycles. We have observed (via analysis) that win objectives are flexible, and the player re calibrates when winning, while loss budgets are indexed to cash loss and are less flexible. In this sense, free-play gives the player more chances to achieve a win objective. The same is conversely not true. Programs that issue too much free-play can actually reduce initial buy-in, hastening a player’s arrival at her cash budget. Likewise, targeting, controls, and choice of casino mgmt system can impact walk rates: a major driver of inefficiency.

Our philosophy on free-play

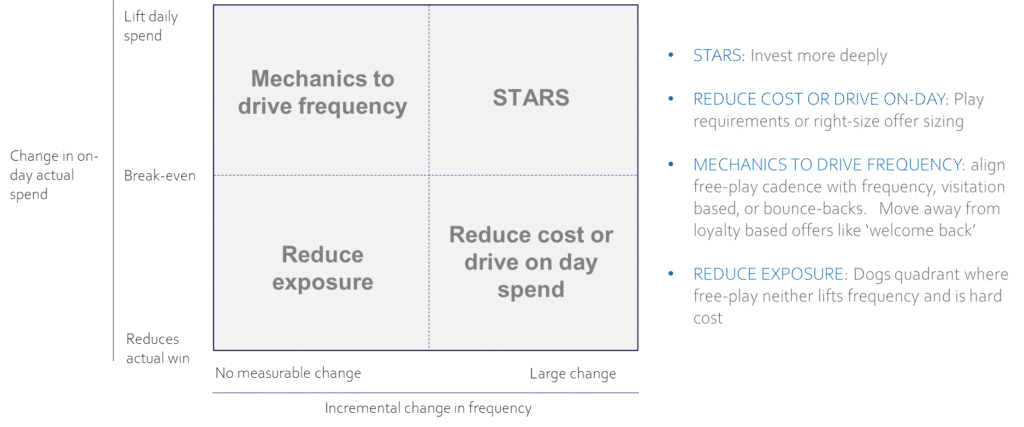

In the previous paragraph, we established that the protagonist of the first part of the slot free-play enigma is on-day spend, which determines the effective cost. As we will see, we are fortunate to recoup the face value of the free-play coupon; thus, incremental lift must come through increased frequency. In working with clients, we have found that high ROI free-play programs excel across these two dimensions. Based on the results of the free-play program we can craft very specific strategies. See the theoretical framework we use for assessing free-play programs in Exhibit One below

At the upper right quadrant of the dogs & stars chart above, free-play increases both on-day spend and changes frequency. We want to invest into this segment and focus on crafting offer mechanics to shifts players into this quadrant.

Free-play actually increases on-day spend but has no impact on frequency among the patrons in the upper left quadrant. There are subtle changes to the monthly / core offer to help drive frequency but this offer is a blunt force object. Instead, we recommend a supplemental offer with personalized targets.

In the bottom-left quadrant, free-play drives frequency but reduces on-day spend. For these patrons we want to experiment with right sizing offer value or creating a personalizes play-based point target.

For patrons in the bottom left hand quadrant, free-play is actually a loss neither driving frequency and materially reducing on-day spend. We should reduce exposure to these segments / patrons.

Analysis

With permission and on the basis of anonymity we analyzed 4 million player-level trip records from four distinct properties within the same portfolio, each located in different U.S. geographic markets and spanning up to five years. Despite these properties being operated by the same entity, we observed considerable variation in issued values, though they adhered to similar SOPs. We only included patrons who had received at least $1 in free-play at some point.

In our analysis, we intentionally included a property that heavily invests in free-play. Echoing the findings of Lucas, we found that the average free-play reinvestment rate (calculated as free-play divided by gross theoretical) ranged from 11% to 30%, with an average of approximately 19%. This figure is inflated due to the inclusion of a property in a competitive market that disproportionately invests in free-play. Subsequently, we segmented the database by value band for further insights.

Analytical framework: Meet faust_

Faust, the central figure in Goethe’s classic, struggles with desperation and an insatiable desire for immediate outcomes, driving him to strike a pact with unforeseen repercussions. This notion of a Faustian Bargain aptly captures the sentiment many operators harbor regarding their free-play programs. The faustian tools within the closed-source version of the CasRISP package is a homage to Goethe’s seminal work. The faustian tools include two key functions:

CasRISP::faust_cost() is a linear estimate of the effective cost for $1 in free-play used. If the faust_cost function outputs a number less than one than the property is not recouping the face value of the free-play coupon. Conversely, if the model output a number greater than one than the free-play increased on-day spend.

CasRISP::faust_freq() estimates the elasticity between frequency and free-play. More specifically, we are estimating via a semi-log regression model the relationship in days between trips given the change in free-play while correcting in player level characteristics.

These functions are intended to be utilized at the segment level and, as with all casino data-science projects, require careful data preparation.

Results

Consistent with previous analyses, we observed minimal to no increase in daily spending across the portfolio. However, our research indicates that under certain conditions, free-play programs can indeed serve as a catalyst for increased frequency. See Exhibit two

On day-spend

Consistent with Lucas’s earlier analyses, we observed modest returns in terms of on-day spend. Across all segments, $1 of free-play increased daily spend by $0.65 to $0.80, translating to an effective cost of $0.20 to $0.35 before taxes. This outcome aligns with expectations, given that the effective cost was indexed to the hold percentage on slot drop but burdened by walk rates. With the average hold percentage on slot drop around 30%, an effective ~20% cost on free-play feels intuitively accurate.

However, the results were far from uniform. The effective range of outcomes varied widely, from $1 in free-play increasing daily spend by $0.38 (a $0.62 cost) to as high as $1.10, indicating that free-play could boost same-day spending. Notably, higher-end patrons showed the most elasticity (their on-day spend changed most relative to free-play value) and incurred the lowest costs. Positive on-day lift was largely confined to a property in a fiercely competitive market, surrounded by rival venues.

A closer examination revealed that large players at this competitive venue were highly elastic, but walk rates surged on days when free-play declined. Management attributed this to large players spending most of their funds at the property with the most attractive offer. This scenario reflects a common challenge across the globe: unwinding right-sized free-play offers is exceptionally painful.

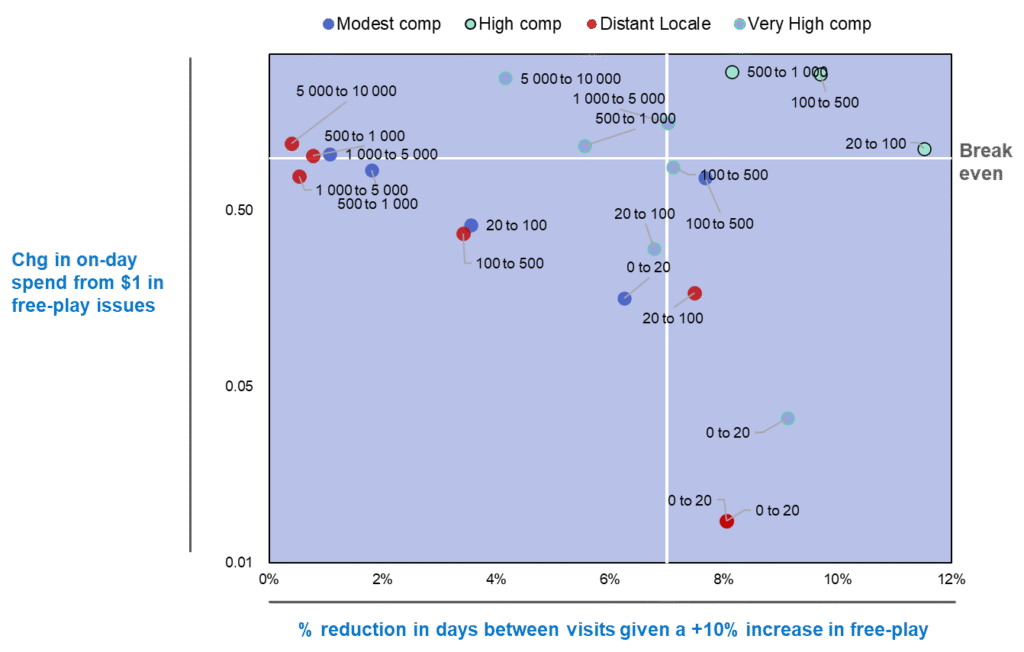

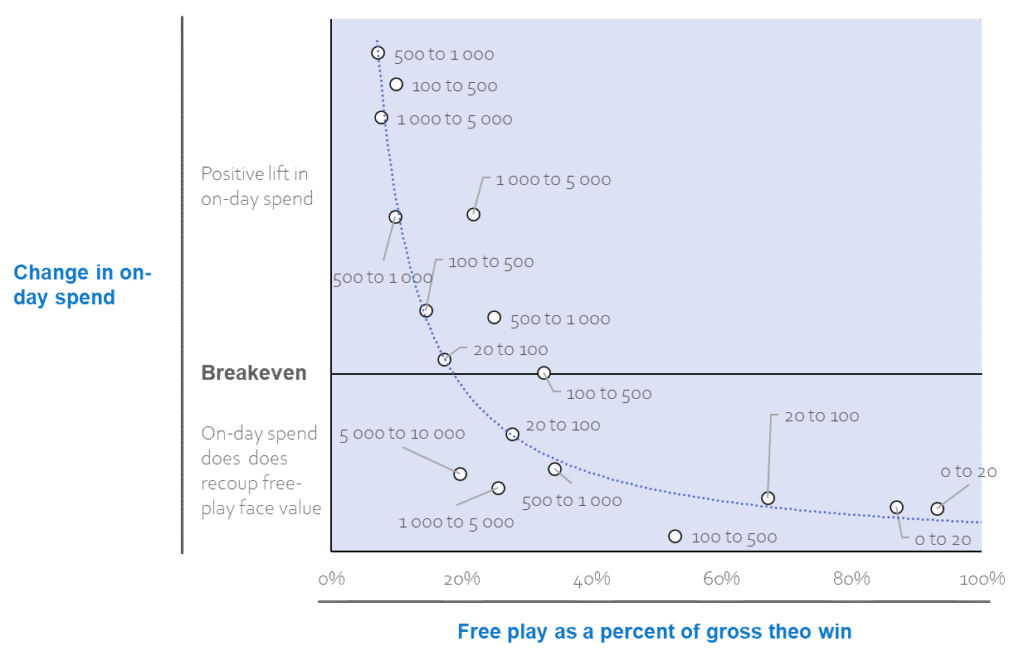

Across markets, we saw the highest costs concentrated in lower-value segments. Typically, entry-level free-play denominations of $5/$10/$20 result in many lower-end players being reinvested at high rates, diminishing their initial buy-in noticeably. This pattern is evident in the provided dataset and has been observed across a range of properties, including an Australian pub operator and an Asian iGaming company. The exhibit below illustrates the relationship between on-day spend per $1 of free-play and the gross free-play reinvestment rate. To avoid the obscuring effect of winning players extending their play time, we only evaluated players who were down on the day.

As highlighted above, the most substantial boost in on-day spending is observed in properties with the leanest free play programs, with incremental gains plummeting as free play offers become more generous. Notably, no property X segment combination yielded a positive on-day lift when free play exceeded 20% of gross theo. In practice, we found only one property where free play reinvestment over 30% did not result in a decline in daily spend.

Although this post does not delve into the matter, readers with an eye on fiscal nuances should explore the tax implications of free play and consult Anthony Lucas’s insightful work on the topic.

Impact on frequency

Our view on free-play programs aligns with many operators: free-play program success is determined not by on-day spend but rather than impact on frequency. In order to correlate the relationship between free-play issued and frequency, we reviewed how changes in free-play impacts the lag between two successive visits. Consequently, we excluded the players first trips and only included players with more than three visits during the analysis period.

In all the property x value segments we reviewed, we found a positive lift, and this result wasn’t random. All but two micro-segments were strongly statistically significant. While the results were statistically valid, this does not mean they were large. Compared to a baseline (median day lag) for each segment, a ten percent increase in free-play reduced the days between visits by seven percent. As with on-day spend, these results varied materially, with idiosyncratic results typically varying by competitive landscape and player value. In general, in competitive and hyper-local markets, free-play has a clear impact on frequency where a ten % increase in free-play drove an 8% to 12% increase in frequency. Higher-value patrons, by contrast, are more difficult to influence. As a general statement: the more competitive the market, the more important the role free-play performs in influencing frequency.

Core monthly offers and lucky money

While academic studies and this analysis find tepid results from free-play, management remains deeply committed with it. In our view, inefficient free-play programs are a secondary consequence of marketing strategies that only loosely influence the desired behaviors. The typical core monthly offer, which accounts for the majority of free-play issued in American casinos, is a blunt instrument. Most of these offers encompass 50 to 100 segments, usually structured along a 2 x 2 grid that covers frequency and monetary value. Some programs adjust patron placement within this matrix based on factors such as proximity to competitors, but the heart remains the same. Each segment is then awarded between one and 12 unconditional tranches of free-play, typically communicated through an overarching calendar that also includes give-aways and tier-based promotions. Despite significant effort spent optimizing the 2 x 2 grid, the segments are ultimately too broad, and the unconditional nature of the offers too diffuse. Instead, we advocate for a more nuanced approach, working with clients to enhance their strategies with personalized, conditional offers designed to elicit specific behaviors.

Waldung, sie schwankt heran, Felsen, sie lasten daran

At the end of Goethe’s eponymous tale, Faust escapes the pact he made with the devil by continuing to persevere towards a goal. In much the same way, we encourage properties to not be resigned to free-play’s inefficiency but rather to continue to evolve free-play programs. In our view, this requires properties to get more personalized and tailor offer mechanics to deliver the desired behavioral changes; of course, doing this at scale requires the adoption of AI.